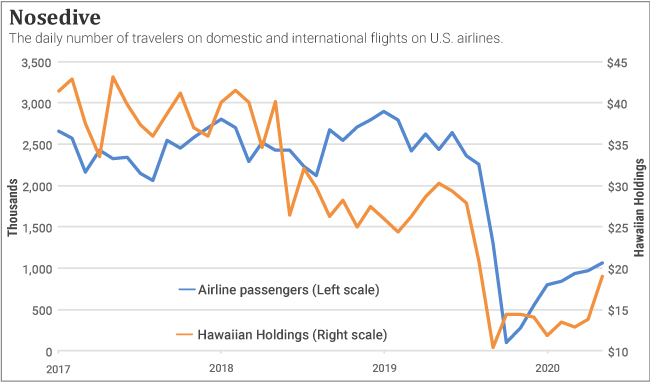

| Nov 23, 2020 Hawaiian Holdings is Ready to Take Off in 2021 Hi Savio, The chart below tells you almost everything you need to know about the global airline industry – both about the devastating downturn it has been suffering, and about the nascent upturn that is now underway.

From an investment standpoint, this chart shows why the airline sector has been one to avoid, and why it may now be one to embrace. At least, that’s why I’m recommending a speculative trade on Hawaiian Holdings Inc. (HA). The investment rationale for Hawaiian Holdings is fairly straightforward: Since the COVID pandemic caused airline travel to plummet; air travel should recover as the pandemic fades into history. Because of the COVID-19 pandemic, the daily tally of passengers flying on domestic and international scheduled U.S. airline flights plummeted from 2.6 million at the start of 2020 to just 100,000 in April. Not surprisingly, airline stocks plummeted as well. But a recovery is underway, despite the COVID crisis. Obviously, humankind has not yet vanquished COVID-19. On the contrary, the pandemic is worsening here in the U.S. and in many other parts of the world. But now that Pfizer Inc. (PFE), Moderna Inc. (MRNA) and other pharmaceutical companies will begin rolling out vaccines, we investors can begin to imagine and end to the pandemic… and to imagine that wayfaring folks will embark on the journeys they have been deferring for nearly a year. To place a bet on reviving air travel, investors could simply buy the U.S. Global Jets ETF (JETS), which holds a basket of domestic and international airline stocks. I expect this ETF to perform very well over the coming 12 months, which is why I recommended it to the readers of Fry’s Investment Report. But in additional to a “shotgun blast” trade like that one, I also like a “rifle shot” trade on Hawaiian Holdings. I expect Hawaiian Holdings to outperform JETS over the coming year, but not because Hawaiian is stronger than the average airline company. To the contrary, Hawaiian’s stock could outperform because the company is weaker than the average airline. Although most airline stocks carry a “junk” credit rating from Standard & Poor’s, Hawaiian’s CCC+ rating is even “junkier” than the ratings of most major airline companies. Hawaiian Holdings’ credit rating has been slipping because the company suffered a double-whammy from the pandemic. Not only did it face the same industry-wide drop in travel that harmed all other airlines, but it also suffered an additional drop because of quarantine restrictions the state of Hawaii imposed on incoming travelers. No other state in the Union imposed and enforced a strict 14-day quarantine. And this law did not just prevent Americans from visiting the islands; it also prevented foreigners from doing so. Hawaiian Air completely cancelled all of its international flights! But because of Hawaii’s strict quarantine law, Hawaiian Holdings devised a nifty work-around that has become instantly successful at promoting travel to the islands. As a result, the airline is likely to generate renewed travel growth, even if the COVID pandemic lingers for many, many months. So far, leisure travel throughout the world is rebounding faster than business travel. But many leisure travelers cannot yet travel to any of their coveted overseas destinations. That’s good news for Hawaiian Holdings. Since the number of tourist destinations open to Americans remains extremely limited, the Hawaiian Islands could become an attractive “fallback” destination. They could pick up a larger share of tourists that want to go anywhere, but cannot yet travel to most overseas destinations. During Hawaiian’s earnings teleconference on October 27, CEO Peter Ingram provided reason for optimism when he discussed the airline’s new program for conducting COVID-free flights: I'm very encouraged that the Hawaii pre-travel testing program, which went into effect on October 15th will mark an important inflection in the trajectory of our business. The program allows the traveler to bypass the mandatory 14-day quarantine by presenting evidence of a qualifying negative COVID-19 test from a state approved provider. The early returns are encouraging. The logistics of the process are going relatively well…We have seen an increase in our load [factor] since the 15th and have seen positive trends in our bookings… The inbound load factor from North America to Hawaii has been running at 57% since the new program started. Bookings for the fourth quarter have been steadily improving as well. But there is no sugar-coating the severity the turbulence Hawaiian Air has been encountering. During the third quarter, total revenue was down 90% year-over-year on an 87% decline in capacity. In North America, Hawaiian operated just 18% of its schedule compared to last year. As a result, the company posted an adjusted net loss of $3.76 per share for the third quarter, compared to a profit of $1.72 in the same quarter last year. But a rebound is underway. During the last few weeks, Hawaiian Air has resumed flights from Portland, Sacramento, San Diego, Las Vegas, Phoenix, San Jose and Oakland, as well as several North America to Maui routes. The company is now flying approximately 36% of its North American schedule compared to last year, and it expects that figure to bump up to the mid-60%s during the coming holidays. Regarding international, CEO Ingram expects to resume flights between Japan and Korea “shortly,” thanks to the fact that the state of Hawaii will include both countries in its pre-travel testing program (as soon as suitable testing partners are secured). Despite the challenging conditions, Hawaiian Holdings possesses significant cash and liquidity to survive them. The company ended the quarter with nearly $1 billion in cash and an additional $577 million in available credit under the CARES Act. Altogether, that’s about two years’ worth of liquidity, based on current conditions. The company’s daily cash burn totaled about $3 million last quarter. But that number is already trending lower and should average about $2.2 million in the current quarter. Looking toward 2021, the company expects to end its daily cash burn halfway through next year and to resume generating positive cash flow. For what it’s worth, 10 Wall Street analysts who follow the company expect it to produce positive cash flow and earnings in the third quarter of 2021. Obviously, earnings estimates for Hawaiian Holdings are essentially wild guesses at this point, simply because the future trajectory and severity of the COVID pandemic is uncertain. Even so, the near-term future for Hawaiian Holdings is not a complete guess. We can see already that airline travel is recovering and that the company’s load factors are trending in the right direction. We can also see that the company has implemented a COVID-free flight program that is unique in the industry, and that could significantly boost travel on its flights, even if the COVID pandemic lasts much longer than we currently expect. Certainly, this stock is speculative. But it is one that could deliver a double over the next 12 months, even if the overall market is going nowhere. Action to Take: Buy the Hawaiian Holdings Inc. (HA) January 2022 $22 calls at $6 or less. The current offered price is $5.50. Use a “limit” order, not a “market” order. Regards,

Eric Fry

The Speculator

|

Comments

Post a Comment