PCE inflation comes in as expected … the falling 10-year yield and softer dollar are helping stocks … can the Fed prevent the unemployment rate from exploding … what to watch Friday No market tantrums after this morning’s inflation report.

The Fed's preferred inflation measure – the core Personal Consumption Expenditures (PCE) Index – showed inflation edged higher in July. But both the headline and core readings were in line with expectations, so the market is marching higher as I write Thursday morning.

The core PCE number that strips out the volatile food and energy components rose 0.2% in July. On a year-over-year basis, core PCE rose 4.2%.

Here’s Bloomberg’s interpretation which is likely similar to that of the Fed: The subdued inflation figures underscore the progress the Fed has made over the past year in taming price pressures.

That said, the central bank is far from declaring victory, and the strength of consumer spending presents a fresh concern for policymakers seeking to ensure inflation continues to dissipate. Bulls can argue the “fresh concern” part. Their counter is that the strong consumer spending is what’s increasing the likelihood of a soft landing.

The bearish perspective is that this bottomless pit of consumer spending actually has a bottom that’s camouflaged by pandemic-fueled savings and skyrocketing credit card balances. But when this bottom arrives, that’s when we’ll face an economic/market reckoning.

For now, this morning’s data didn’t throw us any curveballs, so Wall Street is happy. ADVERTISEMENT Louis Navellier’s Next Big Breakthrough He found Apple in 1988…Cisco in 1992…Oracle in 1990…but on August 28th he jumped on camera and revealed the biggest breakthrough of his career…

Go here now to see this shocking story. Meanwhile, stocks are getting a boost from two key tailwinds The first is falling Treasury yields.

For the details, let’s jump to legendary investor Louis Navellier, editor of Accelerated Profits. From Louis’ Special Market Podcast yesterday: Treasury bond yields have come down quite a bit. The 10-year is now at 4.11%. That’s down dramatically from earlier in the month.

The reason it’s coming down is ADP reported that only 177,000 private payroll jobs were created. That’s a big deceleration from the previous months.

And the JOLTs report – the job openings report – declined quite a bit.

So, everyone is pretty convinced the Fed can’t raise rates, period. Stepping back to fill in the details, let’s follow the daisy chain: 1) “bad news” is “good news” again, which 2) is what the Fed wants, which 3) takes pressure off Treasury yields, which 4) is good for stocks.

As Louis just noted, this week, we’ve received new data showing a marked slowdown in the labor market. We also learned that consumer confidence just fell by the most in two years.

Ordinarily, this would be bad news. But for Wall Street, which is laser-focused on the Fed, this “bad news” suggests that the “data dependent” Fed is getting the result it wants…slowing growth.

And slowing growth increases the likelihood that Powell & Co. will be done hiking rates, which makes all this bad news “good news.”

Tying it to stock prices, the heightened expectation of no more rate hikes bleeds into the Treasury market by pushing up bond prices which lowers bond yields. And as we’ve detailed many times in prior Digests, there’s an inverse relationship between treasury yields (primarily the 10-year yield) and the S&P. So, as yields fall, it serves as a tailwind to stock prices.

You can see this by looking at a chart of the 10-year Treasury yield and the S&P over just the last month.

Below, notice how the surging 10-year Treasury yield (in black) weighed on the S&P’s price (in green) until last week. Since then, the falling yield has boosted the S&P.

The second tailwind for stocks today is a weaker U.S. dollar In the same way that stock prices don’t respond well to surging Treasury yields, neither do they like a strengthening U.S. dollar. As we’ve detailed in prior Digests, a stronger dollar creates currency headwinds for international companies that generate significant revenues overseas.

Below, we look at the U.S. Dollar Index. It’s a measure of the value of the U.S. dollar relative to the value of a basket of six major global currencies – the euro, Swiss franc, Japanese yen, Canadian dollar, British pound, and Swedish krona.

Since mid-July, the dollar has been chugging higher – until the last handful of days.

While it’s premature to proclaim the dollar has hit an inflection point and is now headed lower, we can say that its recent weakness has been helping stocks. ADVERTISEMENT Nothing has grown this fast ever If you think AI’s progress has been impressive, you’re in for a surprise…

AI is improving itself. This is called “reinforcement learning.”

It’s like a baby teaching itself to walk — within minutes. The best way to take advantage of this boom?

The “AI Master Key.” Click here for all the details. This week’s JOLTs labor report puts the unemployment rate in the spotlight From a 30,000-foot perspective, the unemployment rate will make or break the stock market.

That’s because the market is reacting to the Fed’s rate policy… the Fed’s rate policy is dependent on various inflation data … various inflation data are greatly influenced by consumer spending … and consumer spending is largely influenced by the degree to which consumers have good-paying jobs.

Federal Reserve Chairman Jerome Powell has been obvious about the connection between the labor market and Fed policy. Here’s CNBC from after the Fed’s March FOMC meeting: The reason for the continued inflation focus, more than anything else, was always in plain sight: the job market is still too hot and wage growth, while cooling, hasn’t cooled enough for comfort.

Fed Chair Powell’s focus on the labor market has been consistent in the months leading up to Wednesday’s rate hike decision, and when asked at the post-FOMC meeting press conference whether the central bank considered a pause in rate hikes given the concerns about global financial system fragility, his initial response went straight to the labor market.

“Labor market data came in stronger than expected,” Powell said. This week, we’ve gotten cooler labor market data. As we explained a moment ago, this “bad news” is “good news.”

But now, the central question is: “Can the Fed raise the unemployment rate just enough without capsizing the labor market?” History shows it’s tough to keep a lid on rising unemployment once it’s begun Imagine a seesaw with one end resting on the ground. You’re standing on that end, slowing walking toward the elevated end. Your goal is to balance the seesaw perfectly, without accidentally tipping it in the opposite direction.

If you tried this as a kid, you likely recall that once momentum builds in the opposite direction, it can be difficult to stop. Before you know it, the seesaw has inverted.

The Fed faces a similar test with how its rate hikes impact the labor market. What does this look like historically?

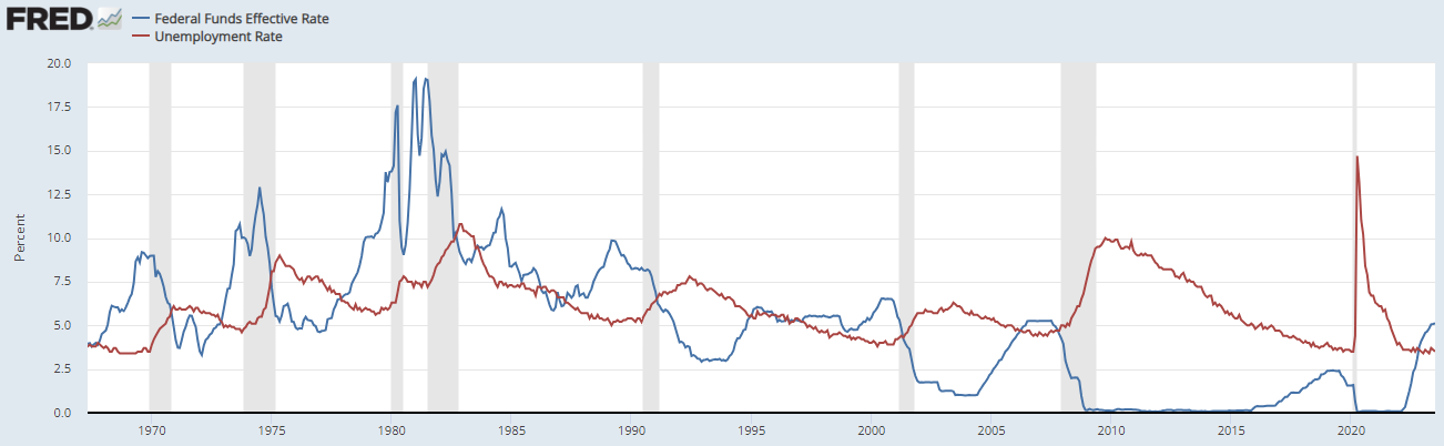

Below, we look at the U.S. unemployment rate dating back to the late-1960s. This is in red.

We’ll also show the Fed Funds Effective Rate in blue.

There are two things to notice…

First, when the Fed Funds Effective rate (in blue) surges to a peak (usually topping out above the unemployment rate in red), we nearly always see a related jump in the unemployment rate in the ensuing months.

It was more exaggerated in the 70s and early 80s, but it remains true in the last two decades.

Second, every single time the unemployment rate (in red) has begun from a level under 4%, the ensuing jump in the unemployment figure has taken the unemployment rate up to 6%+, at a minimum.

There is no example of the Fed being able to delicately nudge the unemployment rate up from, say, 3.6% to 4.2% or 4.8% at which point the rate stabilizes then happily rides off into the sunset.

The closest to that is when unemployment started at 3.4% in 1968 and then jumped to 6.1% in 1970. But even then, after the unemployment rate fell up until 1973, it spiked to 9% by 1975.

(The period from 2000 – 2003 saw inflation top out at 6.3%.)

Bottom line: Unemployment tends to take the stairs down, but the elevator up.

Here’s how this looks.

One more chart for perspective… ADVERTISEMENT The #1 AI Name For 2023 A massive $20.6 trillion wealth shift is underway. And one AI company is igniting this historic move.

It’s backed by the world’s top venture capital firms. Venture Capitalist Luke Lango has just recorded a video with all the details.

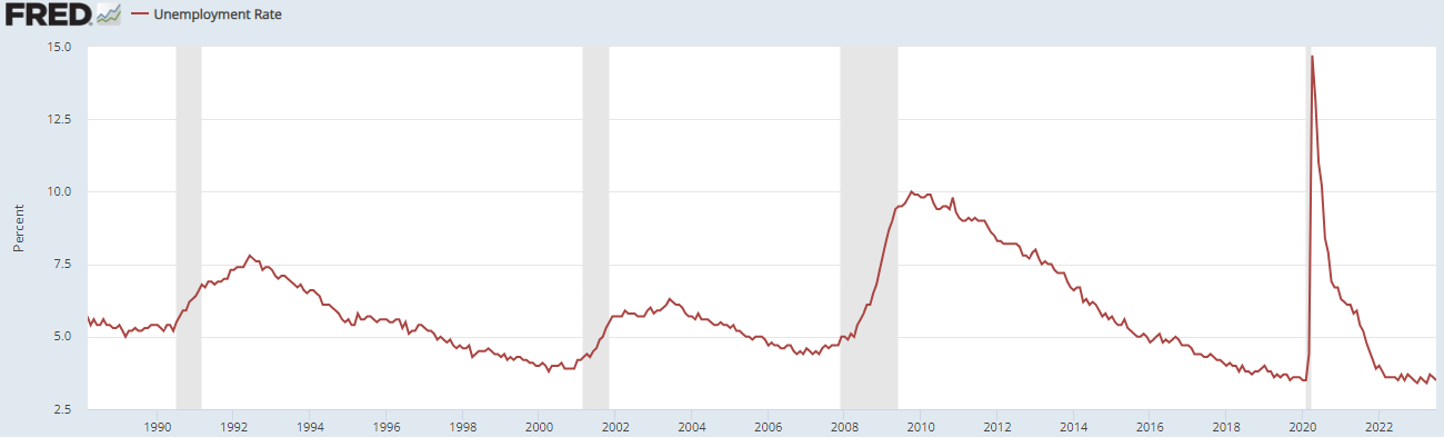

Click here to watch him reveal it now. Below, we’ll zero in on the unemployment rate since 1990 Two things to notice…

First, recognize the “stairs down, elevator up” dynamic we just referenced. In other words, when the unemployment rate finally begins to rise, it’s not a long, gradual incline. Relatively speaking, it’s a fast, steep ascent that’s hard to control.

Second, notice the gray shaded parts of the chart. Those represent recessions.

Since 1990, each time the unemployment rate has climbed from a sub-4% level, a recession followed (and the 2007 recession started from a 4.4% level).  Today, the unemployment rate clocks in at 3.5%.

Yes, this time could be different, but history shows that once the unemployment rate begins to tip the scale, it’s incredibly challenging to stop. Meanwhile, the longer the unemployment rate remains this low, the tighter Fed rate policy is likely to be, increasing the odds they accidentally overdo it.

Pay attention to the Labor Department’s s monthly non-farm payrolls report which comes out tomorrow. It’s the big one that the Fed is watching.

We’ll keep you updated here in the Digest.

Have a good evening,

Jeff Remsburg |

Comments

Post a Comment