Liberty’s Laurels To judge from Liberty’s most recent earnings report, one might think the company is a fast-growing technology upstart from Silicon Valley.

In 2023, the company delivered its second-consecutive year of record earnings per share. For additional perspective, Liberty has tripled its revenue and quadrupled its gross earnings (EBITDA) since becoming a public company in 2017.

During the company’s first four years in the public eye, it averaged $40 million of EBITDA per year. Last year, that number topped $1.2 billion, as earnings per share jumped 49% year-over-year to $3.15.

Clearly, Liberty is doing something right… or many things.

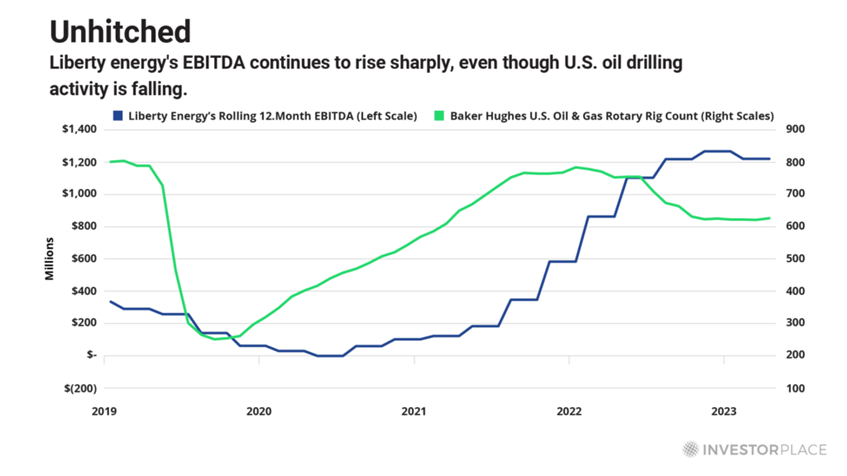

During the last few years, Liberty has been converting its largely diesel-powered frac rigs to a combination of electric and gas-powered ones. At the same time, it is developing the in-house capability to provide a mobile natural gas supply to its gas-powered fleets.

The innovations are creating a fleet that maximizes efficiency, lowers fuel costs, and reduces emissions. Importantly, this unique fleet also attracts robust demand, which is why Liberty’s revenues have been gushing higher, even while the number of operating drill rigs in the U.S. has been dropping.

In other words, Liberty has achieved the enviable ability to prosper, even when the broad oil & gas industry is not.  Riding The Energy Shift The company does not expect a slowdown in the oil patch any time soon. As CEO Christopher Wright explained on the company’s Jan. 25 earnings call… As North American oil production reaches record levels, more frac activity will be required simply to offset production declines… North American operators have been, and are likely to continue to be, the largest provider of incremental oil and gas supply globally. These trends should support a durable, multiyear cycle ahead for [energy] service… We’re going into a less cyclical world than we’ve been in. Wright also presented a fascinating argument for growing long-term oil demand, based on recent demand trends. To summarize, he points out that the so-called “energy transition” is a bit of a misnomer. He asked rhetorically… Are we in the midst of an energy transition that we hear so much about? The data says that the answer is “No.” This is not an opinion or a preference. Heck, I work in other areas of energy and began my career in nuclear and solar. This is simply an honest reading of the data.

In 2010, the world consumed a little more than 500 exajoules of energy. Twelve later, in 2022, the world consumed a little less than 600 exajoules of energy… What energy sources provided this additional energy beyond the 500 exajoules we consumed in 2010?

Oil provided 24% of the growth in global energy, with the large majority of that coming from the American shale revolution. The third-faster growing energy source was coal, which supplied 14% of the additional energy to power our planet. Wind came in fourth at 9%, solar at 7%, and hydro at 4%…

How can we call this a transition where global demand for natural gas, oil and coal continues to grow without even a diminution of market share? Although Liberty is focusing primarily on strengthening its competitive position in the U.S. fracking industry, it is also investing in modest diversifications from that core business.

For example, it has invested in a geothermal energy company called Fervo.

At first blush, this investment might seem far afield from the fracking business. However, the company explains that the same engineering processes that make fracking successful could also make geothermal energy production successful. This venture is not yet producing any revenues, but Liberty continues to advance it.

I’m such a fan of this company that I recommended Liberty to my Fry’s Investment Report subscribers in August 2022. My reasoning then was that it was a technological leader in the energy industry with phenomenal earnings and revenue to back it up. It was also cheap, trading for just eight times 2022 EPS and less than six times the 2023 number.

As I write, the stock is up nearly 50% in the Fry’s Investment Report portfolio… but I believe its run is far from over.

Despite Liberty’s outstanding financial track record and earnings growth, the stock is trading for less than seven times earnings. In other words, investors are treating it like the deeply cyclical energy services company it used to be, instead of the fast-growing technology company it has become.

I think the stock’s valuation significantly understates the company’s growth potential, which is why I still consider the stock a “Buy.”

No company obituary to publish here. Regards,  |

Comments

Post a Comment