Infinite Wisdom, Finite Returns To conduct his study, Gray tracked the hypothetical portfolio only a “god-like” investor could have created by knowing “ahead of time exactly which stocks were going to be long-term winners and long-term losers.”

Spanning from the end of 1926 through the end of 2016, Gray’s researchers computed five-year “look ahead” returns for the 500 largest U.S.-traded stocks, and then split those results into deciles. The top decile (i.e., 10%) contained the 50 stocks that would produce the largest gains over the following five years. The bottom decile contained the 50 worst-performing stocks over the following five years.

Gray’s “God Portfolio” would buy the top decile of five-year gainers at the start of each five-year period, and then rebalance the names in the portfolio on January 1 of every fifth year.

As Gray explains… The first portfolio formation is January 1, 1927 and is held until December 31, 1931. The second portfolio is formed on January 1, 1932 and held until December 31, 1936. This pattern repeats every fifth year…

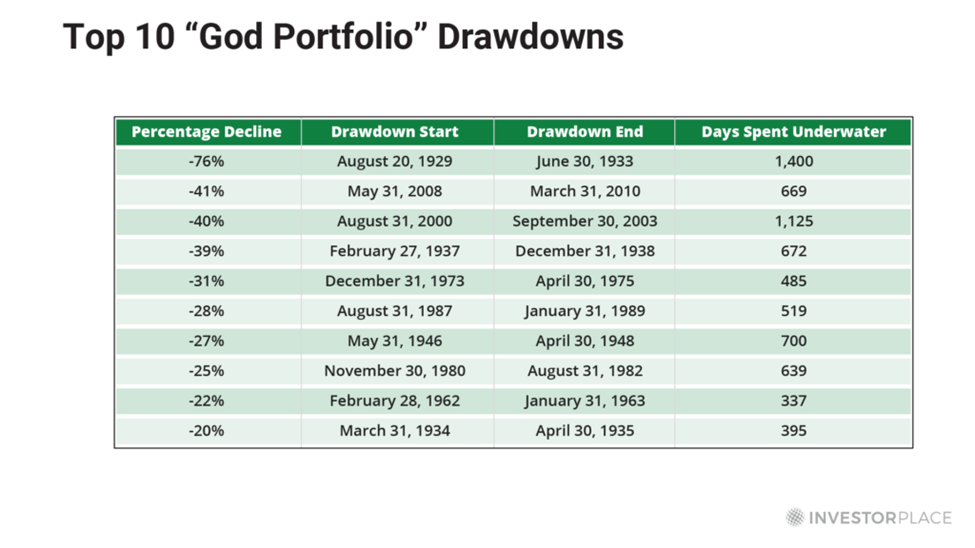

As expected, a portfolio formed on the names that have the best 5-year performance, have the best 5-year performance. Duh. God would compound at nearly 29% a year… but the details are interesting. The “details” to which Gray refers are the shockingly large drawdowns – or mark-to-market losses – the God Portfolio would have endured during its 90-year run.

For example, this “perfect portfolio” would have plummeted 76% from August 1929 to May 1932 and spent nearly four years underwater. Patience Is a Virtue But the pain doesn’t end there. On nine other occasions, the God Portfolio would have suffered drawdowns ranging from 20% to 41%. The chart below details those bumps in the road.  Clearly, a “perfect portfolio” can deliver imperfect results for a time. Even possessing perfect foresight, enduring a 20% drawdown – or 74% drawdown – would not be a pleasant experience. But at least you would know the delightful outcome in advance.

We mere mortals possess no such assurance of “things not seen.” For all we know, a 20% drawdown could become 30%, 40%, or 80%… and it could last for many years. We have no way of knowing.

For example, in my trading service, The Speculator, I issued a buy recommendation in November 2019 on a wireless telecommunications company called Aviat Networks Inc. ( AVNW) – a 5G play.

Aviat Networks is a leading global provider of microwave networking solutions that enable communications networks to handle multi-gigabit data flows. Specifically, Avia provides equipment that high-speed wireless “backhaul links” use to transmit large volumes of data to more centralized nodes for processing and routing, as well as the modular switch hardware those nodes require.

In other words, Aviat provides exactly what 5G networks need in order to transmit and route large amounts of data quickly.

Just four months later, Aviat had slumped nearly 50% to nearly $3 per share. However, given its fundamentals and growth trajectory, I expected AVNW to move up substantially. So, we sat tight and waited for the stock to rebound.

And boy did it rebound.

AVNW began to turn around in May 2020 and has not looked back since. Since my recommendation, the stock is now up a whopping 370%! (Learn more about The Speculator and how to subscribe by going here… and if you’re already a The Speculator subscriber, you can click here to log in to our members-only website now .)  So, the only thing we can know with relative certainty is what we own, not where it’s headed.

We can never know what others will pay for it tomorrow. But if what we own is valuable, and is ultimately increasing in value over time, others will recognize that value eventually… and pay for it.

So, that basic strategy, coupled with dividends – which produced half of the S&P 500’s total return over the last 30 years – is the essence of successful investing.

No God-like qualities needed. Making the Juice Worth the Squeeze The bottom line: Finding and buying excellent companies is the “secret” behind every successful investor’s strategy. Timing helps, but it isn’t everything. As Warren Buffett famously remarked, “It’s far better to buy a wonderful company at a fair price, than a fair company at a wonderful price.”

We investors must also have the strength of conviction to hold excellent stocks, even when they do not perform brilliantly at the outset and/or when popular opinion turns against them.

Holding on to “losers” is not comfortable… and does not always produce immediate success. But if you're invested in a good stock, then the juice is often worth the squeeze.

Regards, |

Comments

Post a Comment