ADVERTISEMENT

According to a recent study, there are over 1,500 new crypto millionaires being minted every single day thanks to the current rally. Thanks to a new project by Luke Lango and his team, you could soon be one of them.

Get the details here

Even God Would Get Fired as an Active Investor

Eric’s latest issue of Investment Report highlights a research piece by Wesley Gray, the CEO/CIO of Alpha Architect, who has a PhD in finance from the University of Chicago.

Gray’s piece is entitled “Even God Would Get Fired as an Active Investor.”

Let’s begin with Eric providing some context:

To conduct his study, Gray tracked the hypothetical portfolio only a “god-like” investor could have created by knowing “ahead of time exactly which stocks were going to be long-term winners and long-term losers.”

Spanning from the end of 1926 through the end of 2016, Gray’s researchers computed 5-year “look ahead” returns for the 500 largest U.S.-traded stocks, then split those results into deciles.

The top decile (i.e., 10%) contained the 50 stocks that would produce the largest gains over the following five years. The bottom decile contained the 50 worst-performing stocks over the following five years.

Gray’s “God portfolio” would buy the top decile of five-year gainers at the start of each five-year period, then rebalance the names in the portfolio on Jan. 1st of every fifth year.

As Gray explains in his paper, the results are what you would imagine. This heavenly portfolio produced fantastic five-year performance – a yearly return of nearly 29%, to be exact.

But camouflaged by that fantastic, overall return are some alarming details.

Back to Eric:

[Underneath the 29% average annual returns are] shockingly large drawdowns – or mark-to-market losses – the godly portfolio would have endured during its 90-year run.

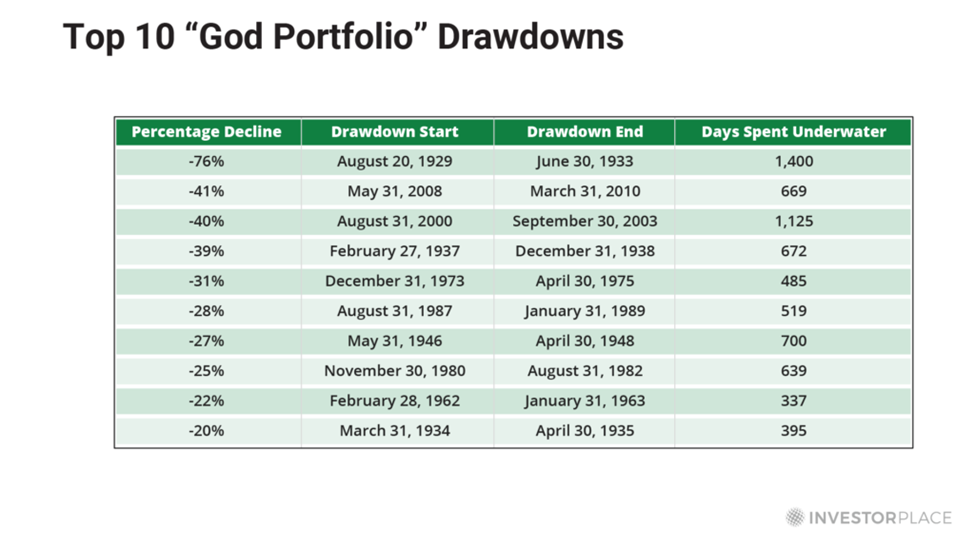

For example, this “perfect portfolio” would have plummeted 76% from Aug. 1929 to May 1932, and spent nearly four years underwater.

But the pain didn’t end there.

On nine other occasions, the God portfolio would have suffered drawdowns ranging from 20% to 41%. The chart below details those bumps in the road.

Clearly, a “perfect portfolio” can deliver imperfect results for a time.

As Eric points out, it’s one thing to suffer through a 20% drawdown (not to mention a 74% drawdown) knowing the delightful outcome you’d eventually enjoy. But obviously, we don’t have that confidence.

As far as you and I know, a 20% drawdown could become 30%, 40%, or 80%… and it could last for many years.

Back to Eric:

We can never know what others will pay for [the stock we own] tomorrow. But if what we own is valuable, and is increasing in value over time, others will recognize that value eventually, and pay for it.

That basic strategy, coupled with dividends, is the essence of successful investing.

Timing Isn’t Everything

Here’s a hypothetical…

Let’s say you find a great company, maybe it even pays a fat dividend. But then you buy at precisely the wrong time. Say, the height of the Dot Com market bubble…

That would be a fatal error, right?

Perhaps, perhaps not.

In his issue, Eric asked his readers to consider a range of investments beginning on Mar. 31, 2000.

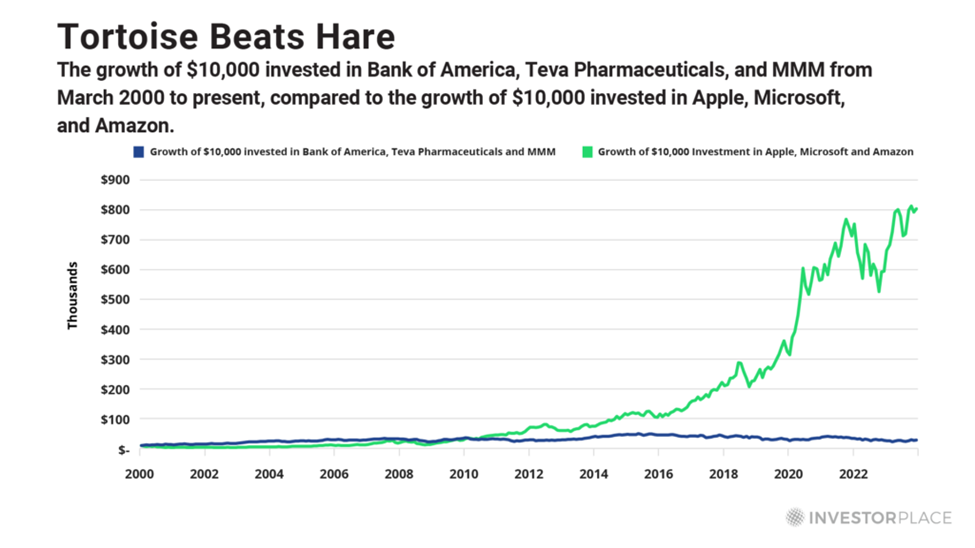

Specifically, “Investor A” spends $10,000 to buy a three-stock portfolio that holds equal amounts of Amazon.com Inc. (AMZN), Microsoft Corp. (MSFT), and Apple Inc. (AAPL). Eric calls this the “Future Leaders Portfolio.”

On that same date, “Investor B” spends $10,000 to buy a three-stock portfolio that holds equal amounts of Bank of America Corp. (BAC), Teva Pharmaceuticals Industries Ltd. (TEVA), and 3M Co. (MMM). This is the “Current Leaders Portfolio.”

Here’s Eric with the results:

Four years later, Investor B’s $10,000 would have grown to $24,261 in the Current Leaders Portfolio, while Investor A’s $10,000 would have shriveled to just $5,058 in the Future Leaders Portfolio.

But this illustration does not end in 2004.

Look what happens when we extend the analytical timeframe another 20 years to the present day.

Over the entire timeframe – from Mar. 2000 to Mar. 2024 – $10,000 grows to just $27,832 in the Current Leaders Portfolio, but skyrockets to $804,489 in the Future Leaders Portfolio.

But during the dark days of 2004, a result like this would have seemed unimaginable.

In that miserable moment, the Future Leaders Portfolio had spent the previous four years slashing a $10,000 investment in half.

Imagine you’re the owner of that Future Leaders Portfolio in that moment. Would you be able to hold?

Think realistically – facing, say, a child’s college tuition, or a home down payment, or a shriveling retirement savings account – would you be able to ride through a 50% drawdown?

Even if so, consider the stress and second-guessing that would likely leave you tossing and turning at night.

Back to Eric:

In the world of professional investing, any money manager who dared to allocate heavily to stocks like Microsoft, Amazon, and Apple during the early 2000s would have been fired long before 2004, if not also sued for daring to buy such pathetic “underperformers” like those.

But as Eric points out, short-term setbacks are not foolproof indicators of future results.

Most investors would penalize even perfection

In his research paper, Gray made a tweak.

To highlight the futility of prioritizing short-term results over long-term success, he converted the perfect “God portfolio” into a perfectly hedged God portfolio.

Gray tracked the results of buying the God portfolio, while simultaneously hedging it by selling short the lowest decile of future 5-year performers.

This “perfect” hedge fund would have produced a spectacular compound annual growth rate (CAGR) of 46%. No one has ever achieved a return like that over a prolonged period.

But here’s Eric with the twist:

[Despite this unbelievable market performance], as Gray points out, “God would get fired multiple times over.”

Why? Because the hedged God portfolio would have spent large periods of time “underperforming” the benchmark S&P 500 Index.

On multiple occasions, the God “hedge fund” would produce a return that trailed the S&P 500 by more than 50 percentage points!

The following quote comes directly from Gray’s paper:

The relative performance of God’s hedge fund is often abysmal… The [S&P 500] index would eat His lunch on multiple occasions…

These results highlight the fickle nature of assessing relative performance over short horizons…

Investors must have a long horizon!

What’s your conviction level when you find a strong company?

As Eric’s issue emphasizes, investors must have the strength of conviction to hold excellent stocks, even when they do not perform brilliantly at the outset and/or when popular opinion turns against them.

Of course, most investors lack such conviction. I’ll add in how the yearly results of the Dalbar studies illustrate this.

You’ve likely heard of the Dalbar studies. Since 1994, this investment research firm has published its Quantitative Analysis of Investor Behavior (QAIB) report that measures the stock market performance of the average retail investor.

As you might expect that performance is not great.

Consider the period from 1992-2022. This 30-year stretch covered the Dot-Com bubble/crash, 9/11, Global Financial Crisis, COVID pandemic and the bear market of 2022). Despite all this, the S&P 500 delivered an average annual return of 9.65%.

And how did the average U.S. equity mutual fund investor do over the same period?

According to Dalbar, thanks to our tendency to get scared and bail on stocks at the bottom and become greedy and buy stocks at the top, the average investor made just 6.81% per year. That’s nearly 30% less than the S&P 500.

Back to Eric:

We all know the phrase, “Buy low; sell high.” But too often we do the exact opposite because we lack the confidence to stay the course.

We get spooked out of a great stock, simply because its price falls for a while, and/or public opinion turns against it.

We allow our doubts to overrule our judgment…

Sometimes, of course, we misjudge the stocks we own. We bravely cling to a stock we believe to be a long-term winner, only to discover down the line that it was no such thing. We were simply wrong. That happens… to all of us.

But more often, our doubts are traitors.

ADVERTISEMENT

Wall Street legend has just uncovered one tiny Maryland company that could become the next Nvidia. Few in the media are talking about this story yet… but in the next 6 months that’s all they’ll talk about.

Go here now for this breaking story.

What’s your tendency? Do you listen to your doubts and fears or evaluate the strength and/or weakness of your stocks?

In his issue, Eric zeroed in on Amazon in the wake of the Dot-Com bust when investors were punishing its stock price.

He noted that from March 2000 to March 2004, Amazon’s revenues tripled, while its annual net income flipped from a negative $1.5 billion to a positive $156 Million.

And how did Wall Street reward that brilliant performance?

By mass selling that crashed Amazon’s share price as much as 90%.

Imagine you were an Amazon investor during this period. Maybe you’d be able to hold if you remained focused on this operational excellence. Even then, it’s doubtful.

But if you had been focused on Amazon’s plummeting stock price? I’d give you a near-zero chance.

We’re running long so I’ll begin to wrap this up

Who knows what the coming weeks/months/years will bring for the market and your specific portfolio.

But as Eric’s issue stresses, your long-term wealth will come from the combination of fantastic companies and patience. But don’t expect that to be easy.

Consider the typical tradeoff…

Following your emotions in the short-term often feels the best, but results in disappointing long-term performance.

Meanwhile, following discipline and logic in the short-term usually feels the worst, but often provides far better long-term performance.

This echoes the quote from Rob Arnott, founder of Research Affiliates:

In investing, what is comfortable is rarely profitable.

Back to Eric’s issue:

We abandon stocks that have great potential, simply because we expect too much too soon, and/or we believe that short-term price declines foreshadow long-term price declines.

I call this type of mistake the “Tyranny of the Immediate.”

This tyranny that prioritizes short-term results over long-term potential. It demands being right, right now. By doing so, it often sabotages the opportunity to capture large long-term gains.

Eric provides a handful of examples, one of which his Speculator subscribers experienced not too long ago.

In November 2019, Eric recommended a trade on Aviat Networks Inc. (AVNW). Just four months later, the position had slumped nearly 50%.

Today, the subscribers who acted on Eric’s initial recommendation and held through that drawdown would be sitting on a 400% gain.

To what extent are you at risk of allowing the Tyranny of the Immediate to derail your long-term wealth creation?

I’ll let Eric take us out:

Even legendary stocks will try the patience and endurance of investors from time to time… en route to delivering their market-trouncing returns…

Holding onto “losers” is not comfortable… and does not always produce immediate success. But the juice is often worth the squeeze.

Have a good evening,

Jeff Remsburg

Comments

Post a Comment